Outstanding Receivables Are a Capital Allocation Decision

Most cannabis brands aren't short on revenue. They're short on liquidity.

When tens or hundreds of thousands of dollars in delivered product sit on net-30, -60, or even -90 terms, that capital is tied up in your retailer's payment timeline. For a finance team managing production cycles, payroll, and retail expansion simultaneously, that allocation has downstream costs that compound across every outstanding invoice on the books.

Nabis Capital is a tool for reclaiming that allocation. Like the late, great J.G. Wentworth once said, it’s your cash, and you need it now.

The Cost of the Status Quo

Across Nabis, 70 days (40 days late and the average 30-day net terms) is the average days sales outstanding (DSO), in California and New York.

A brand carrying 65 outstanding invoices at any given time, with an average order value of $2,500 each, is sitting on $162,500 in inaccessible working capital. Not in funding your production run, not supporting new account onboarding, and not expanding marketing and advertising.

At the average DSO, that capital only turns approximately five times per year. The difference between deploying it and waiting on it is the difference between a capital-efficient operation and one that is perpetually catching up.

Nabis Capital closes that gap, at a cost that, for most brands, is significantly lower than the alternative of constrained growth or external debt.

What Nabis Capital Is

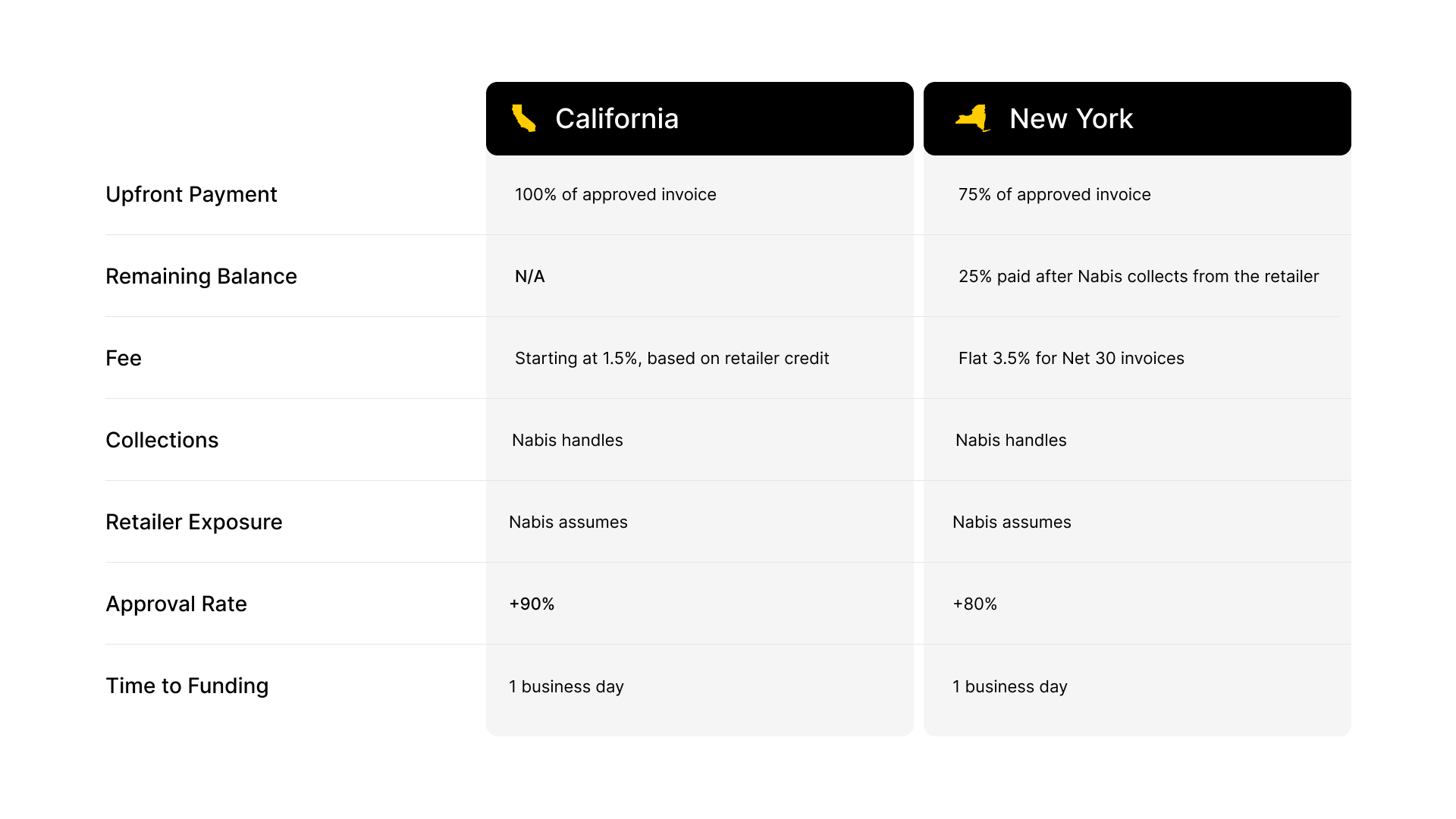

Nabis Capital is an invoice financing program available to brands distributing through Nabis. When a qualifying invoice is approved, Nabis pays that invoice value directly to the brand within 1 business day.

Across both California and New York, when using Nabis Capital, Nabis will manage retailer collections and assume all credit exposure. If the retailer doesn't pay, the brand keeps the funds.

Nabis Capital launched in Q3 2020. Since then, 70 brands have been funded, with $50M+ in total volume deployed and approval rates that have remained stable across both markets.

How to Get Started

- Reach out to the Nabis Capital Team.

- Confirm that your accounts receivable are not assigned as collateral for other debt, and you have the right to sell them to Nabis.

- Sign the Factoring contracts.

Then, follow these three simple steps:

- Submit a delivered Nabis invoice to the Nabis Capital team.

- Receive an approval decision on your invoice.

- Funds are deposited within 1 business day.

Nabis manages retailer collections from that point. There are no bank relationships required, no personal guarantees, and no lengthy applications. Eligibility is assessed at the invoice level.

Brands can submit one or multiple invoices at a time through a structured workflow, with a simple submission process that integrates directly into their existing operations.

Contact the Nabis Capital team to find out which of your current invoices qualify.

What It Looks Like in Practice

In practice, this can be a one-time event or a recurring part of how many brands manage working capital.

A New York-based cannabis brand with an average payment delay of ~40 days submits invoices for funding on a near-daily basis, often immediately after delivery. Rather than waiting over a month to collect, they consistently access capital 4–6 weeks earlier, effectively converting receivables into immediate liquidity.

In some cases, where payment delays extend significantly longer, the benefit is even more pronounced—turning what could be months-long delays into next-day access to capital.

Get Paid on What You've Already Earned

The receivable is on your books. The capital is yours. Nabis Capital moves the payment timeline to match the work already completed.

Contact capital@nabis.com to find out which of your current invoices qualify.

Frequently Asked Questions

What is Nabis Capital's invoice financing for cannabis brands?

Nabis Capital invoice financing lets a brand access the cash value of an unpaid invoice before the retailer pays it. Rather than waiting 30-, 60-, or 90-days for payment on delivered product, the brand receives most or all of the invoice value upfront minus fees from a financing partner, in this case, Nabis, who then collects directly from the retailer.

Why can't cannabis brands use traditional bank financing?

Most cannabis brands are ineligible for conventional business financing due to federal restrictions on cannabis. Banks operating under federal charter cannot service cannabis businesses in most circumstances, which means the standard tools available to other CPG brands, including lines of credit, revolving facilities, and invoice factoring through major financial institutions, are largely inaccessible. That structural gap is what Nabis Capital is designed to fill.

What is the difference between invoice factoring and invoice financing?

The terms are often used interchangeably, and the practical difference is narrow. Invoice factoring typically involves selling an invoice outright to a third party, who then owns the receivable and collects payment directly from the customer. Invoice financing may involve the invoice as collateral for an advance, with the brand remaining responsible for collection. Nabis Capital functions as an invoice factor. Nabis purchases the receivable and handles all collections, with no recourse to the brand if the retailer doesn't pay.

How does Nabis Capital work?

You submit a delivered Nabis invoice to the Nabis Capital team. If it qualifies, you receive payment within 1 business day. After fees, brands receive 100% of the invoice value in California and 75% upfront in New York, with the remaining 25% paid after Nabis collects payment from the retailer. Nabis assumes responsibility for the collection process and credit risk.

What does non-recourse mean, and why does it matter?

Non-recourse means that if the retailer fails to pay, Nabis absorbs the loss, not the brand. The funds paid to the brand are not clawed back.

What percentage of invoices get approved?

Over 90% of submitted invoices are approved in California. In New York, the approval rate is over 80%. Approval is based on the retailer's credit profile, not the brand's financial history or internal credit standing.

Is Nabis Capital available to my brand?

Nabis Capital is available to all brands. Approval for invoice submissions is based on invoice eligibility. To find out whether your invoices qualify, reach out directly to the Nabis Capital team at capital@nabis.com. Eligibility is assessed at the invoice level, so even if you haven't used the program before, it's worth a conversation with the team.

Does Nabis Capital require a credit check or personal guarantee?

No. There is no personal guarantee, no bank relationship required, and no lengthy application process. Approval is based on the invoice and the retailer's credit, not the brand's credit history or the personal finances of its principals.

Does Nabis Capital have any minimum fees or minimum volumes required?

No. Nabis Capital has no minimum fees or minimum invoice volumes required to submit for invoice factoring.

.jpeg)

.png)